![]()

You Pty Ltd: Running Your Finances for Maximum Profitability

Looking at your personal investment set-up objectively uncovers major problems which could compromise your financial health. Borrowing from the wisdom of the corporate sector can teach us a few things about how to structure our finances in the most profitable way.

Imagine your family was a listed company on the Australian Stock Exchange, John & Mary Smith Pty Ltd, for example. Both husband and wife would be the Chairman of the Board and the Chief Executive Officer (CEO), and they would also be the shareholders who own the company.

If your family balance sheet was a company balance sheet, your home might be your biggest asset, and all your other investments – including your super fund, would also be assets.

Anything you owed money on, like your mortgage or the car repayments, would be liabilities.

Your job is to manage the company so as to build the assets and maximise the returns on your investments, while keeping the liabilities under control and in line with your assets and cashflow, so that the company stays in the black and the share value increases.

Ignoring the obvious differences in size and income, what do you think is the major difference between BHP, Westpac and you? Especially when speaking in terms of structure and management style?

The answer is that large listed companies have a very formal management structure and every one in it has their own well-defined job to do, unlike the family structure where it’s a different story.

In a large listed company, the CEO (Chief Executive Officer) is responsible for the day-to-day management of the company. He advises the Board on investment opportunities and reports to them regularly on progress. And he is held responsible for delivering the profit which he has undertaken to deliver each year.

When it comes to day-to-day decisions on running the company, the Chairman doesn’t tell the CEO what to do, but he does have the power to fire him.

If the Chairman and his Board think the CEO isn’t taking the business where it needs to go and is not giving the shareholders a fair enough return on their money, the Board fires the CEO and appoints a new one. This is the decision making process in any public listed company.

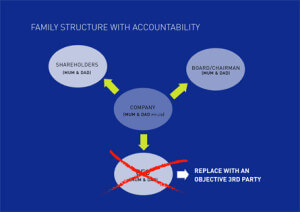

Now compare this very formal structure with your own family ‘listed company’. The shareholders who own the family business are Mum and Dad. The CEO who has to make the day-to-day decisions on saving, spending and investing the family income is Mum and Dad. And the Chairman who has to ensure that the CEO makes a proper job of it is, once again, Mum and Dad. In other words, they have made the decision to let themselves make all the decisions. That’s the problem with most family’s financial planning. There is no clear-cut responsibility for the success of the investment strategy and the Chairman, CEO and Shareholders are accountable to no one except themselves.

The most important thing that’s wrong with the majority of household wealth creation strategies is that they are managed by the wrong people. In fact, the first thing you should do as Chairman, if you do want to manage your family finances professionally, is fire yourselves as CEO and employ someone else with professional investment skills to do the job. In the context of the family company the CEO would probably be a professional financial adviser.

In this new structure, Mum and Dad are still the shareholders and get the profits, and they are also still the Chairman, but they have outsourced a lot of the financial decision-making to an external CEO who is accountable to them. This ensures accountability and objectivity, while still leaving you in control of your own finances and your own destiny.

You will naturally hire your own CEO, carefully choosing someone who impresses you. But the truth is that whoever you hire as CEO, you will probably have a better chance of investment success than if you continued to be your own CEO, Chairman and Shareholder, all rolled into one.

And of course, as the Chairman, if at any point you don’t like the job your CEO is doing, you can sack them and employ someone else as CEO.